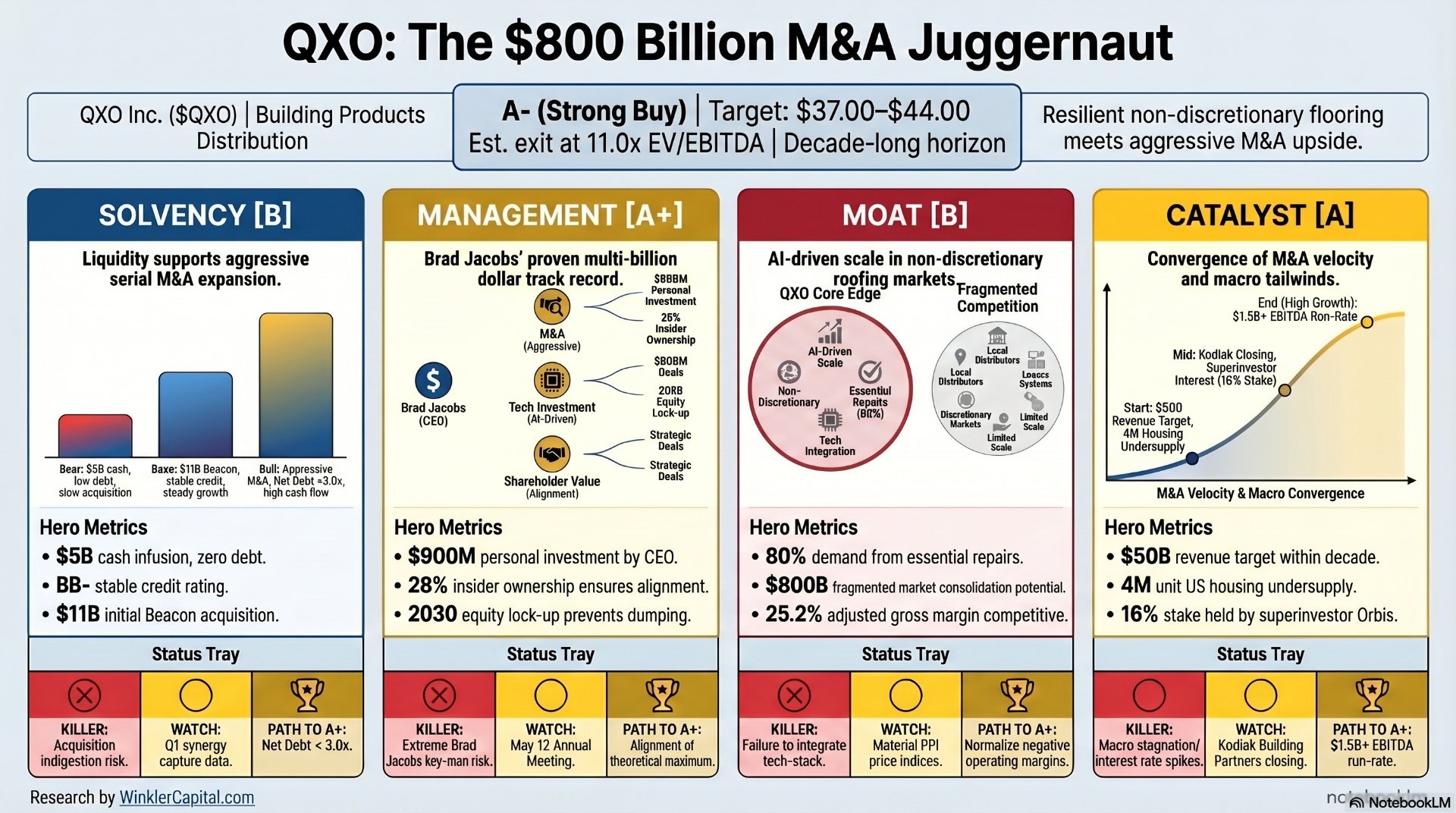

Executive Summary

Strategic Consolidation and Value Uplift

In the high-stakes arena of industrial distribution, the emergence of QXO Inc. represents a paradigm shift in the application of the "Serial M&A" playbook. This professional-grade 4-Pillar Deep Dive, synthesized for the Winkler Capital investment rubric, evaluates whether QXO stock possesses the foundational solvency, management pedigree, structural moat, and fundamental catalysts required to deliver outsized alpha in the $800 billion building products distribution market.

Full video: https://youtu.be/XKBXCbBFVCE

Final Verdict Grade: A- (Strong Buy)

Primary Risk (Thesis-Killer)

M&A Overpayment & Bidding Wars: The entry of Home Depot (GMS acquisition) and Lowe's (Foundation Building Materials) into the distributor M&A space creates a risk of "multiple creep." If QXO$14.25+0.85% is forced to pay >12x EBITDA for future acquisitions, the "accretive" engine stalls, and interest rate sensitivity could turn the current debt into a "debt trap" if housing starts remain depressed through 2027.

Monitoring List

- Kodiak Closing: Early Q2 2026 (Confirmation of the $1B EBITDA run-rate).

- Earnings Date: May 7, 2026 (First look at post-Beacon organic trends).

- Macro: Monthly Census Bureau construction reports (Looking for a reversal of the 0.3% decline).

Exit Trigger (The "Summited" State)

Exit the position when QXO reaches its $50 billion revenue run-rate target or achieves a 20% valuation premium over Ferguson (FERG) on an EV/EBITDA basis, combined with a sustained 15% ROIC. This would signal that the business has transitioned from a growth-by-acquisition story to a matured, dominant market leader.

Pillar 1: Solvency (The Foundation)

Solvency is the non-negotiable floor for the Winkler Capital framework. In the case of QXO$14.25+0.85%, the firm has undergone a high-velocity transformation from a $5 billion cash shell into a multibillion-dollar distributor via the $10.5 billion acquisition of Beacon Building Products. While the capitalization table has expanded rapidly, the solvency analysis must determine if the "Survival Runway" is sufficient to support Brad Jacobs' aggressive "buy-and-build" strategy through a cyclical housing downturn.

The "Floor": Balance Sheet & Quasi-Debt Analysis

As of December 31, 2025, QXO’s liquidity position is substantial but complex. We must look beyond headline debt to the full liability stack:

- Cash Position: $2.36 billion.

- Long-Term Debt: $3.06 billion.

- Quasi-Debt (Liquidation Preference): The balance sheet carries $558.1 million in Mandatory Convertible Preferred Stock and $498.6 million in Convertible Preferred Stock. These instruments represent a combined $1.06 billion in seniority over common equity, effectively bringing the "debt-like" burden to over $4.1 billion.

- Total Liabilities: $6.18 billion against total assets of $15.89 billion. However, $8.93 billion of the asset base consists of Goodwill and Intangibles, which lowers the tangible floor significantly. In addition, most of the debt matures on April 30, 2032, allowing significant time to pay off and refinance in case lower rates arrive (i.e. Warsh).

Triangulated DCF Analysis

Our valuation bridge uses the following three scenarios to test the $800 billion fragmented-market opportunity. To evaluate the "Floor" of the security, we employ a triangulated DCF model using a hurdle rate of 9.2% (R—— = 0.092$) to account for the current "BB" credit risk profile and the capital-intensive nature of industrial roll-ups.

1. Bear Case: The "Liquidation" or "Stagnation" Scenario

In this scenario, we assume the "Jacobs Playbook" fails to integrate acquisitions effectively. Organic growth remains flat (0% terminal growth), and margins fail to expand beyond the legacy roofing industry averages of 7%. This scenario identifies the value of the underlying assets (warehouses, fleet, inventory) minus the debt load.

- Assumptions: Terminal growth 0%, Adjusted EBITDA margin remains stuck at 6.9%

- Implied Value: $14.20 per share. This represents the "liquidation" value floor, where the market ceases to pay any premium for management expertise or future M&A.

2. Base Case: The "Conservative Execution" Scenario

This scenario contemplates growth in line with the broader building products sector (GDP + 2%) and moderate margin expansion as the company integrates Beacon and Kodiak. It assumes QXO achieves approximately half of its $50 billion revenue target within the decade.

- Assumptions: 10-year revenue CAGR of 18.5%, Adjusted EBITDA margins expand to 9.5%.

- Implied Value: $28.50 per share. This scenario reflects the intrinsic value of a well-run industrial distributor without assuming a "tech-premium" valuation.

3. Bull Case: The "Optimized Turnaround" Scenario

The Bull Case assumes full execution of the $50 billion revenue target and the realization of a 500-basis point margin expansion driven by "tech-enabled" procurement and AI-driven inventory management.

- Assumptions: 10-year revenue CAGR of 26.5%, Adjusted EBITDA margins reach 12%

- Implied Value: $44.10 per share. This reflects the "Summit" state where QXO is valued as a market leader alongside peers like Ferguson or Watsco.

Survival Runway

The FY 2025 Net Loss of $(279.4) million is an accounting artifact of the Beacon integration, suppressed by $314.7 million in amortization and $83.7 million in transaction costs. The Adjusted EBITDA of $647.8 million provides ample coverage for the $138 million in annual interest payments.

- Solvency Risk Verdict: No. With $2.36 billion in cash and a 2.7x Net Debt/Adj. EBITDA ratio (pro-forma for the $1B run-rate), QXO is well-capitalized.

Section Grade: B

The Path to A+

To reach a perfect grade, QXO must deliver a Free Cash Flow (FCF) to Total Debt ratio of >15%. Currently, integration cap-ex and transaction fees are clouding the FCF profile; a move to A+ requires pro-forma FCF to stabilize above $600 million against the $4.1 billion total debt/preferred stack.

Pillar 2: Management (The Jockey)

Distribution is a scale game where the "Jacobs Playbook" excels: consolidating fragmented industries to leverage procurement power and proprietary tech.

The Serial Compounder

Brad Jacobs (who just released his new book 'How to Make a Few More Billion Dollars') is a "Fixer" with an unparalleled track record, having completed 500 M&A transactions and scaled five multibillion-dollar firms. His stated strategy is not "growth for growth's sake" but rather the creation of "outsized stockholder value." Per his December 11, 2023, launch statement, his focus remains on "accretive M&A" and "improving margins and generating high returns on capital."

Incentive Alignment & Dilution Analysis

Management alignment is Tier 1. The initial $1 billion cash investment included $900 million from Jacobs Private Equity (JPE) and $100 million from Sequoia Heritage. However, the cost of this "strategic fueling" is significant. In 2025, QXO executed a $4.25 billion common stock offering, driving the weighted-average share count from 204 million to 613 million. This 200%+ dilution is only justifiable if the ROIC on the Beacon/Kodiak acquisitions exceeds the cost of capital (estimated at 10-12%).

Incentive Structure: Vanity vs. Value

Transcript data confirms Jacobs' focus on "accretive capital allocations." In earnings calls, management has emphasized "margin expansion" and "sales force effectiveness" over raw top-line targets. This suggests an focus on ROIC milestones rather than vanity metrics.

| Incentive Metric | Management Commitment/Detail | Impact on Shareholders |

| CEO Personal Investment | $900 Million (90% of initial round) | Extreme "Skin in the Game" |

| Insider Ownership % | Brad Jacobs owns ~28% of equity | Total alignment with price appreciation |

| Performance-Based Comp | 2/3 of equity tied to TSR > 55th percentile S&P 500 | No payout for "Average" performance |

| Sale/Transfer Lock-up | Restricted through January 1, 2030 | Prevents "Pump and Dump" behavior |

| Open Market Purchases | No discretionary sales; only tax withholding events | Signal of long-term holding |

Section Grade: A+

The Path to A+

N/A. Current alignment is at the theoretical maximum for a public company.

Pillar 3: Moat (The Horse)

QXO aims to bridge the gap between a traditional commodity distributor and a tech-forward leader.

Margin Bridge & Accrual Normalization

QXO’s 2025 Adjusted Gross Margin (24.9%) and Adjusted EBITDA Margin (9.5%) compare favorably to Builders FirstSource (10.4% EBITDA margin) and Ferguson (9.4% operating margin). Critically, QXO’s GAAP margins were suppressed by a $131.7 million inventory fair value adjustment. Normalizing for this non-cash hit reveals a platform that is already operating at peak industry efficiency despite being in the early stages of integration.

Structural Advantage: The Tech Lever

The moat is predicated on the "nascent use of technology" in the $800 billion industry. While competitors rely on legacy ERPs, QXO is building a "blank canvas" platform focused on AI-driven price optimization and automated inventory management. With B2B e-commerce expected to triple by 2030, QXO’s tech-first approach creates a switching-cost advantage for contractors requiring real-time jobsite visibility.

Cyclical Durability

Despite a 0.3% decline in January 2026 construction spending and a "below-normal starts environment," QXO’s unit economics are protected by the structural 3-million-unit U.S. housing shortage. In a $2.2 trillion total construction market (SAAR), QXO only needs a 2.3% market share to hit its $50 billion revenue target—a low bar for a consolidator of this caliber.

| Company | Gross Margin (LTM) | EBITDA Margin (Adjusted) | Operating Margin |

| QXO Inc. | 24.2% | 6.9% | -3.6% |

| Ferguson (FERG) | 31.0% | 10.4% | 8.9% |

| Core & Main (CNM) | 26.9% | 12.2% | 12.2% |

| Watsco (WSO) | 28.0% | 11.3% | 10.0% |

Section Grade: B

The Path to A+

To achieve A+, QXO must achieve a total market share of 5% across North America and Europe while demonstrating an Adjusted EBITDA margin of 12%, signaling that its tech stack provides genuine pricing power over legacy peers.

Pillar 4: Catalyst (The Kick)

We are entering the "Accumulation" phase of the cycle, where structural undersupply outweighs short-term rate sensitivity.

Macro & Institutional Forces

The 3-million-unit housing deficit is the "Rising Tide." Institutional validation is high, led by the $1.2 billion Apollo Global Management investment. Notably, QXO was absent from Carl Icahn’s Q4 2025 portfolio. We interpret this as a positive: the absence of an activist means the "Kick" is purely execution-led by Jacobs, without the noise of a forced proxy battle.

View the APPENDIX for Macro charts

Momentum Trigger: The Kodiak Re-Rating

The Q2 2026 closing of the $2.25 billion Kodiak Building Partners acquisition is the primary trigger. This deal triples the TAM to 200 billion and establishes a **1 billion EBITDA run-rate**.

- Implied Price Target: If peers like Ferguson (FERG) trade at ~12x-14x EBITDA, QXO’s $1 billion run-rate implies an Enterprise Value of 12B-14B. After adjusting for debt, this targets a stock price re-rating to the 28-30 range upon closing.

The Alpha Thesis

QXO is the superior vehicle over BLDR or FERG because it lacks "legacy baggage." While BLDR must navigate an 11.2% net sales decline (Q4 2025), QXO is growing by acquisition into a vacuum. It is a "pure-play" on M&A velocity.

Section Grade: A

The Path to A+

The transition to A+ requires a Q2 2026 earnings beat following the Kodiak close, specifically demonstrating $50 million+ in immediate "synergy capture" through procurement consolidation.

Appendix

"If demographics are destiny, the demographic born in 1990 and 1991 was destined to compete for housing, jobs and other resources. Those two birth years, the people set to turn 33 and 34 in 2024, make up the peak of America’s population." - NYT

"More recent new construction hasn’t replaced America’s graying housing stock, meaning the age of the median home is a record 44 years, according to the Harvard Joint Center for Housing Studies." - WSJ

"The US has a shortage of at least 10 million single-family homes, according to a new report from White House economists" - Bloomberg

"President Donald Trump signed two executive orders in March in an effort to show action on the issue. One of them is aimed at easing access to mortgage credit and directs the Consumer Financial Protection Bureau to tailor mortgage rules to make it easier for smaller banks to “facilitate more affordable lending,” according to a White House fact sheet. The second is designed to ease environmental rules to speed up development and infrastructure projects." - Bloomberg

Homeownership is below the norm for the largest population group, mean reversion would give way to massive buying of homes - WhiteHouse

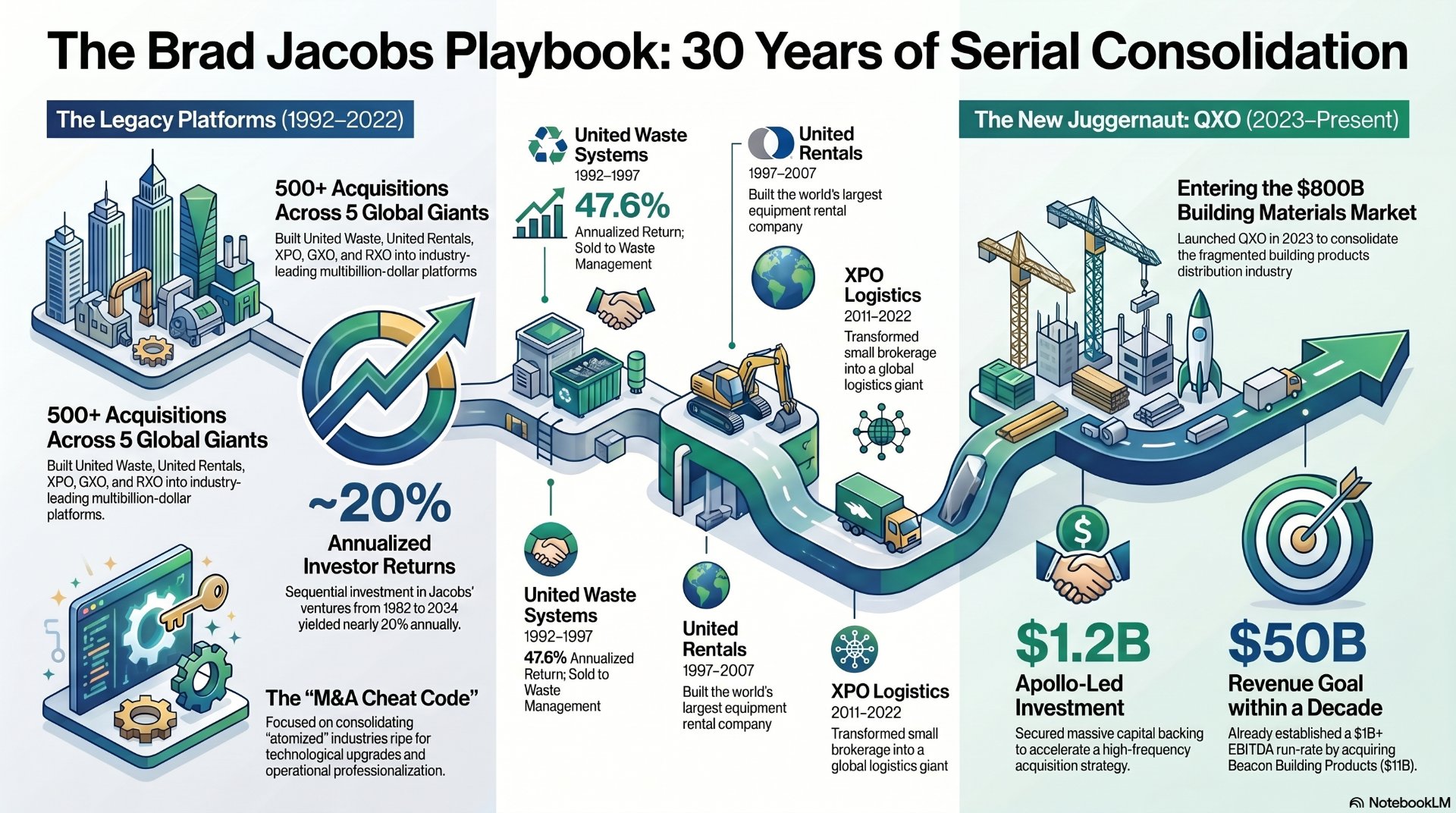

Brad Jacobs is widely regarded as a master of the "Serial M&A" playbook, having built five multi-billion dollar, publicly traded companies from scratch before launching his current venture, QXO. His strategy centers on identifying large, fragmented industries and consolidating them through aggressive acquisitions, technological optimization, and high-performance talent.

The Historical Track Record

Over a 30-year period (1992–2024), an investor backing Jacobs' ventures would have realized an annualized return approaching 20%. His prior successes include:

- United Waste Systems (1989–1997): Jacobs consolidated the fragmented waste industry, which was then dominated by local "mom and pop" operators. He improved margins by implementing methodical route planning and technology. The company was sold to USA Waste (now Waste Management) for approximately $2.2 billion, delivering a 47.6% annualized return to shareholders.

- United Rentals (1997–2007): He targeted the equipment rental industry, building it into the world's largest rental company. He utilized data science and acquired the software provider Wynne Systems to optimize asset utilization and pricing. During his tenure, the company delivered an 8.2% annualized return while the S&P 500 remained flat.

- XPO, Inc. (2011–2022): Jacobs transformed a small truck brokerage into a global logistics giant. He invested heavily in technology, moving an industry that primarily used phones to digital transactions (now 97% digital at the brokerage spin-off RXO). XPO produced a 24.4% annualized return, inclusive of its major spin-offs.

- GXO & RXO (2021–2022): Under Jacobs' leadership, XPO executed two massive spin-offs in less than 15 months: GXO Logistics (the world's largest pure-play contract logistics provider) and RXO (a leading tech-enabled freight brokerage).

The "Brad Jacobs Playbook" Strategy

Jacobs' approach is defined by several core pillars that he is now applying to the building products distribution industry through QXO:

- Fragmented, Large Industries: He targets "atomized" sectors with hundreds of billions in annual revenue, where no single player dominates. The building products industry has approximately $800 billion in annual revenue and over 7,000 distributors in North America alone.

- Technological Alpha: He enters industries with low digital penetration and implements "tech-forward" platforms to lower costs and improve customer service. He views technology as the primary differentiator between industry "haves" and "have-nots".

- Speed and Scale: Jacobs has completed approximately 500 acquisitions in his career. His teams utilize a standardized integration playbook to manage multiple large acquisitions simultaneously.

- High-Performance Culture: He prioritizes recruiting "superlative people" who possess intelligence, hunger, and integrity. He famously leads with an intense work ethic, often operating on minimal sleep during major deal cycles.

The Current Play: QXO, Inc.

Launched in 2024 through the recapitalization of SilverSun Technologies, QXO aims to reach $50 billion in annual revenue within a decade. Within its first year, QXO established itself as a major player by:

- Acquiring Beacon Roofing Supply for $11 billion in April 2025.

- Agreeing to acquire Kodiak Building Partners for $2.25 billion in early 2026.

- Raising over $9 billion in capital from blue-chip institutional investors like Apollo Global Management and Temasek.