Video: https://youtu.be/OYv48HvUOpA

Executive Thesis

The core lesson regarding dividends is that market complacency at all-time highs often leaves high-quality "Consumer Staples" deeply out of favor, creating a rare window for "bond-replacement" yields and long-term capital appreciation.

Macro Factors for Dividend Investors

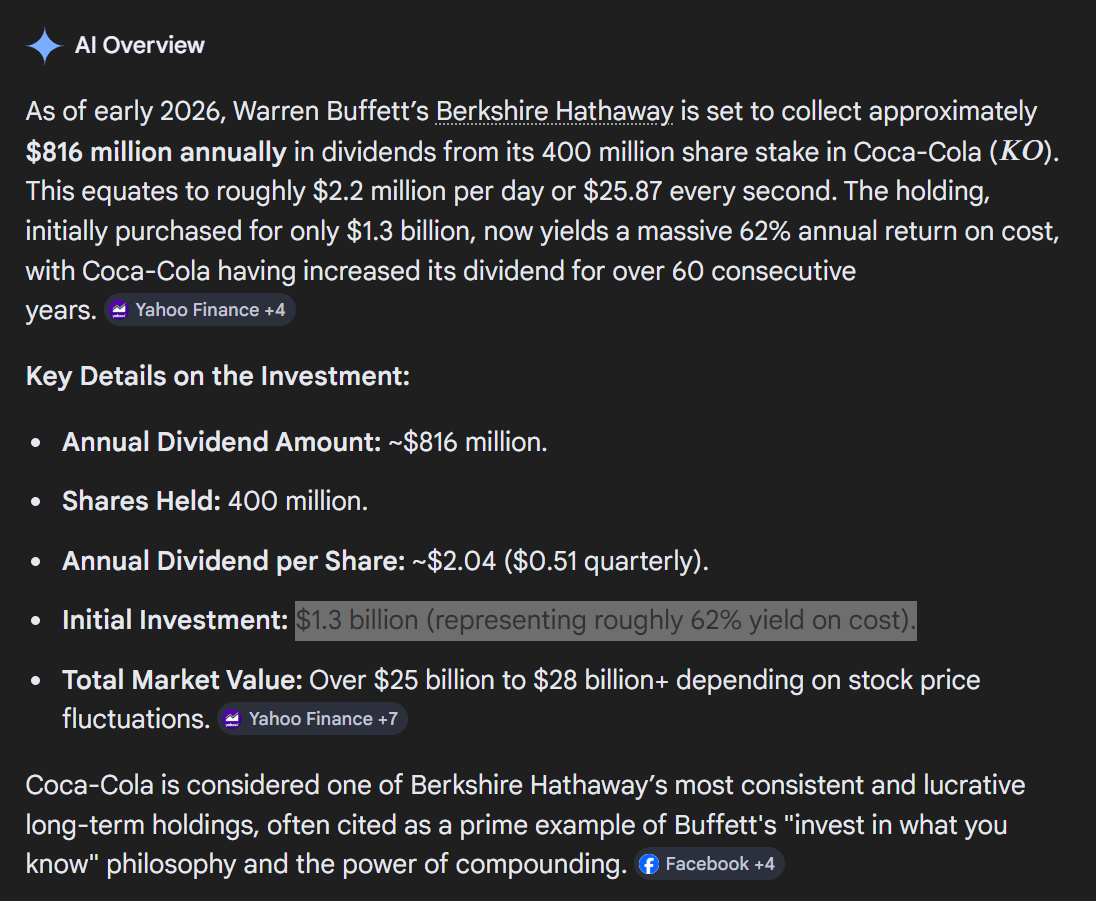

- Yield on Basis vs. Dividend: The "Warren Buffett Coca-Cola" lesson. By buying quality companies when their yields are historically high (due to low stock prices), your "yield on basis" can grow to 15–20% over 10–14 years as the companies continue to raise their dividends annually.

The "Yield on Cost" (YOC)

This is the most important concept for long-term wealth. Yield on Cost is the dividend yield calculated using your original purchase price, not the current market price.

Example: The 10-Year Horizon

- You buy a "hated" staple at $20 with a $1.00 dividend. Your yield is 5%.

- Fast forward 10 years. The company has performed well and raised the dividend every year. The dividend is now $2.50.

- The stock price has also recovered and is now $50.

- The "Current Yield" the public sees is 5% ($2.50 / $50).

- BUT... your Yield on Cost is 12.5% ($2.50 / $20 original price).

This is how Warren Buffett earns a roughly 50% yield on his original cost for Coca-Cola (KO$83.49+1.04%). He isn't getting a special deal; he just bought it decades ago at a low price and the dividend kept growing.

- The "Warsh" Catalyst: With the anticipated appointment of Kevin Warsh as Fed Chair, we expect a regime shift toward rate cuts. This will cause investors to "clamor" for dividend payers, driving up stock prices as yields normalize.

- Inflation: Staples as "Bond Proxies"; however, high-quality Staples have pricing power, allowing them to grow nominal dividends to outpace inflation over time

- Input costs: Spikes in raw materials (aluminum, grains, energy) and freight during the Iran conflict have temporarily crimped gross margins

- GLP-1 (weight-loss drug): An exaggerated fear of mass adoption of weight-loss drugs (Ozempic/Wegovy) will lead to a permanent, terminal decline in caloric intake, destroying demand for snack and processed food portfolios

This "trifecta of fear" has driven valuations to 20-year lows. We argue these fears are not reflected in the actual cash flows, making the current sector "despondent" and thus a "generational buy".

Quick Terms

Dividend Per Share (DPS): This is the actual dollar amount the board of directors agrees to pay you. If the company pays $0.42 per quarter, the annual DPS is $1.68.

Dividend Yield: This is the percentage calculation: (Annual DPS / Stock Price) * 100

Individual Dividend Stock Picks

Here is a "basket" of staples that he views as superior cash replacements:

| Ticker | Company Name | Yield | Analysis / Lessons |

| CAG$13.78+1.25% | Conagra Brands | 9.8% | Historically yields 2-3%. If the dividend compounds at 5%, your yield on basis doubles in 14 years. Brands like Slim Jim and Healthy Choice are "durable". |

| CPB$22.73+1.70% | Campbell Soup | 7.8% | A "complete dumpster fire" currently, which we love. Includes Goldfish and Pepperidge Farm; cash flow per share is steady despite sentiment. |

| GIS$35.40+1.72% | General Mills | 7.0% | Expected to provide a 14% yield on basis a decade out, alongside a likely double or triple in the stock price. |

| HRL$24.81+1.43% | Hormel Foods | 5.6% | Core Holding: A "Dividend Aristocrat" with a 10% return on capital. We see a margin turnaround ahead. |

| CLX$95.27-0.12% | Clorox | 4.75% | Historic yield is 2.2%. Despite private label competition, We view it as a "needed" brand that will recover its margins. |

| MKC$50.92-3.65% | McCormick | 3.57% | Historic yield is 1.8%. You are getting a "double yield" because the price is down. |

| DEO$85.16+2.50% | Diageo | N/A* | New Pick: Trading at 12x forward earnings (cheapest since GFC). New CEO Dave Lewis ("Drastic Dave") is "kitchen-sinking" the quarter and cutting costs. |

| BTI$58.95-1.78% | British American Tobacco | N/A | Mentioned in passing as a high-conviction dividend play that is "unbelievably cheap". |

*Diageo recently cut its dividend to a floor of 50c to "right-size" for the turnaround.

The "Safe Money" Strategy

We concluded that for investors with significant cash, buying these "boring" companies when no one wants them provides a 12% blended yield and a capital triple over a decade, far exceeding the returns of sitting in a 5% money market fund that will soon see lower rates.

Appendix

From: https://bilello.blog/2026/the-week-in-charts-4-17-26

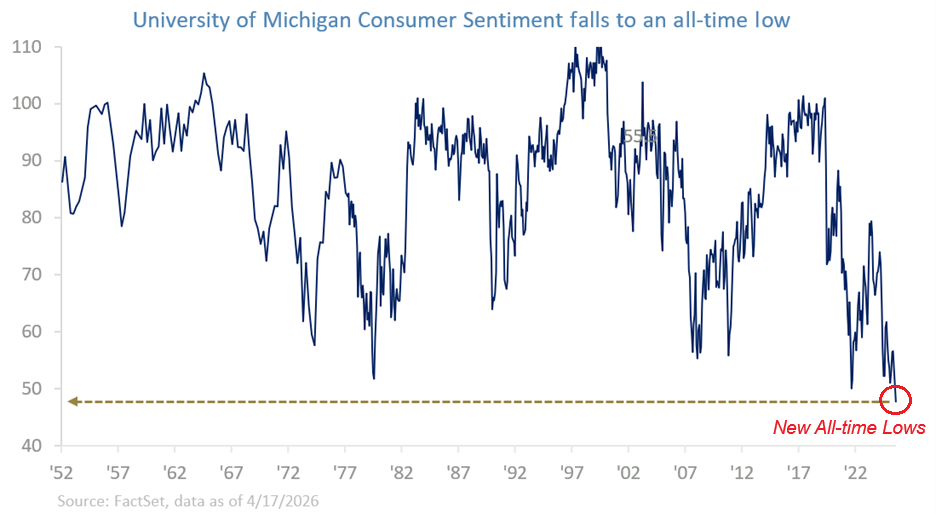

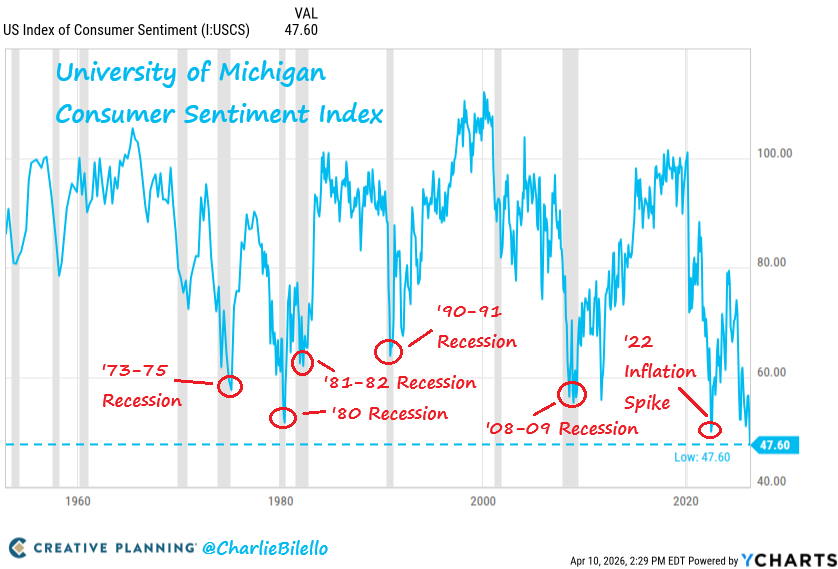

The US consumer sentiment index from the University of Michigan goes back to 1952. Incredibly, it has never been lower than it is today. This is a period that includes the stagflationary 1970s recession, the Global Financial Crisis and the covid downturn.

Why are consumers so gloomy?

Substantial increases in their concerns over high prices. This much is clear: consumers really, really hate inflation. But the question, of course, is do they hate it enough to reduce their discretionary spending? That remains to be seen.

---

"The University of Michigan Consumer Sentiment Index just broke down to new all-time lows" - TendLabs